[ad_1]

Picture illustration of U.S. Dollar, Swiss Franc and British Pound bank notes taken in Warsaw, January 26, 2011. REUTERS/Kacper Pempel/File Photo

WASHINGTON (Reuters) – The world economy was kept afloat by huge spending by governments during the pandemic. Officials mobilized a fiscal response unlike any since World War Two to boost household incomes and give businesses a chance to survive the crisis.

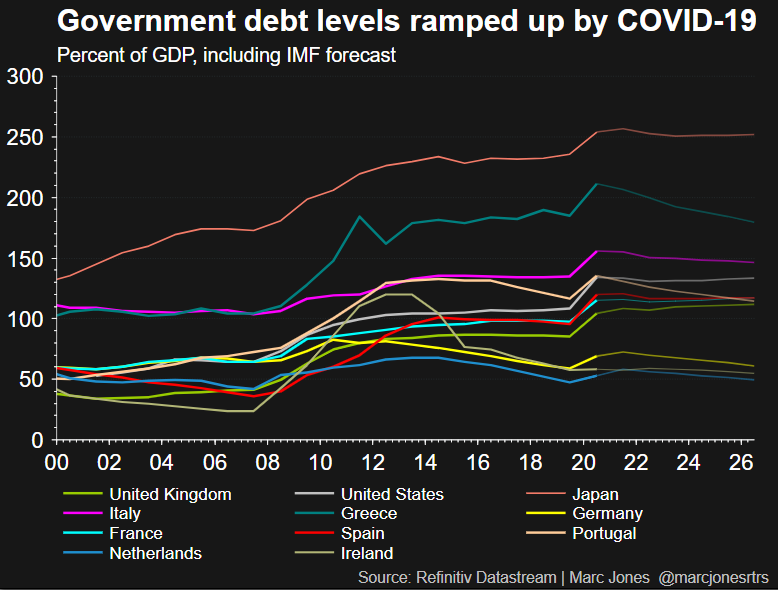

However, the nearly $300 trillion in debt that will result from this massive pile of debt by households, businesses, and governments will leave many countries with fragile finances that will impede efforts to address urgent issues like climate change and aging populations.

Even though rich and poor governments are taking stock of their finances, inflation is forcing central banks to raise interest rates and tighten monetary policy. This, for the indebted can only make the math less favorable.

Emre Tiftik, director of sustainability research at the Institute of International Finance, the global association of financial industry professionals, stated that this would mean higher borrowing costs and higher interest burdens for both the government as well as the real sectors.

“Over the medium-term, the issue is about finding the resources for climate goals and most of them are extremely behind on this,” he said. He also spoke of the urgent decarbonization of global economies that is necessary to avoid a climate catastrophe.

This month’s Glasgow climate talks resulted in some new pledges from countries to lower carbon emissions. But many questions remain about how these commitments will actually be funded and implemented.

According to the IIF global debt may have just about reached its peak after the pandemic, and may fall slightly by the year’s end from $296 trillion at the moment.

However, to reduce our dependence on carbon-based energy and mitigate climate damage, massive public and private investments will be required – estimated at $90 trillion by 2030 according to one World Bank estimate.

At this point, there is no global plan on how to underwrite it. The government’s share of climate investments will have competition with social, healthcare, and other spending priorities, which will increase due to demographic trends like the ageing population.

The huge pandemic stimulus provided by the rich world supported their economies and was sustainable in an environment of low or very low interest rates. As the cycle shifts to tightening policy, this will lead to higher interest costs, greater risk of debt crises in emerging market countries, and less ability to meet climate goals.

“The balance between benefits and costs of debt accumulation has become increasingly tilted towards cost,” Brookings Institution scholars wrote last month. They cited possible constraints to policy and “crowding-out” of private investment.

GOING PRIVATE?

According to Amar Bhattacharya, a London School of Economics professor, low-income countries will be hardest hit. Some already have unsustainable debt levels, while others are locked out of more favorable financing that is available to wealthier countries.

He said that the cost of servicing debt is high, which can impact on climate ambitions and climate vulnerability. He called for more efforts to restructure debt in these countries.

Contrary to this, developed countries can finance their debts in domestic currency at low rates. The U.S., Europe, and other countries have central banks that have an almost unlimited capacity to absorb debt and create reserves.

According to U.S. Congressional Budget Office projections, U.S. debt service cost as a percentage of gross domestic product will rise only modestly over the next decade from 1.6% in 2020 to 2.7% by 2031. This is despite overall debt reaching 106% of GDP. In previous years, this would have triggered alarm bells.

Jason Furman, an economics professor at Harvard University, stated that the most advanced economies are not facing a lot of debt constraint. He has tried to shift the debate about public debt so that the discussion focuses more on servicing costs and less the total amount.

But it is politically sensitive, prompting Congressional representatives to trim President Joe Biden’s climate investments. There’s still the chance of disruption from an abrupt change in Federal Reserve policy and the potential impact that could have on global financial markets if Congress fails or is delayed in raising the U.S. national debt ceiling.

Europe is currently going through its own balancing act. EU capitals are discussing how to relax rules that require governments to keep deficits below 3% GDP and debt below 60%.

Most people agree that those restrictions are unrealistic and would require debt cuts which are too ambitious to support economic growth in most EU countries.

This is why there was such fervor in Glasgow at Mark Carney’s announcement by the U.N. climate ambassador that banks and institutions with $130 trillion of total private capital had declared combating climate change a priority.

However, critics raised concerns about whether all that money was really going to create a net-zero-carbon world. It was clear, however, that governments of all income levels will need to figure how they do most of the heavy lifting regardless of any debt they may be facing.

According to the LSE’s Bhattacharya, this webinar might help to focus attention on one thing: if there is no investment now to manage the growing climate impacts on our economy, then the world’s current debt will only get worse.

He stated, “That investment is best for actually assuring long term debt sustainability.”

Reporting by Howard Schneider, Mark John; Additional reporting by Marc Jones; Graphics by Marc Jones; Editing: Leslie Adler

Our Standards The Thomson Reuters Trust Principles.

{kind=link}