[ad_1]

A surge in China’s output of carbon dioxide (CO2) in the second half of last year pushed the country’s emissions above their 2019 total, despite the impact of the coronavirus pandemic, new analysis for Carbon Brief shows.

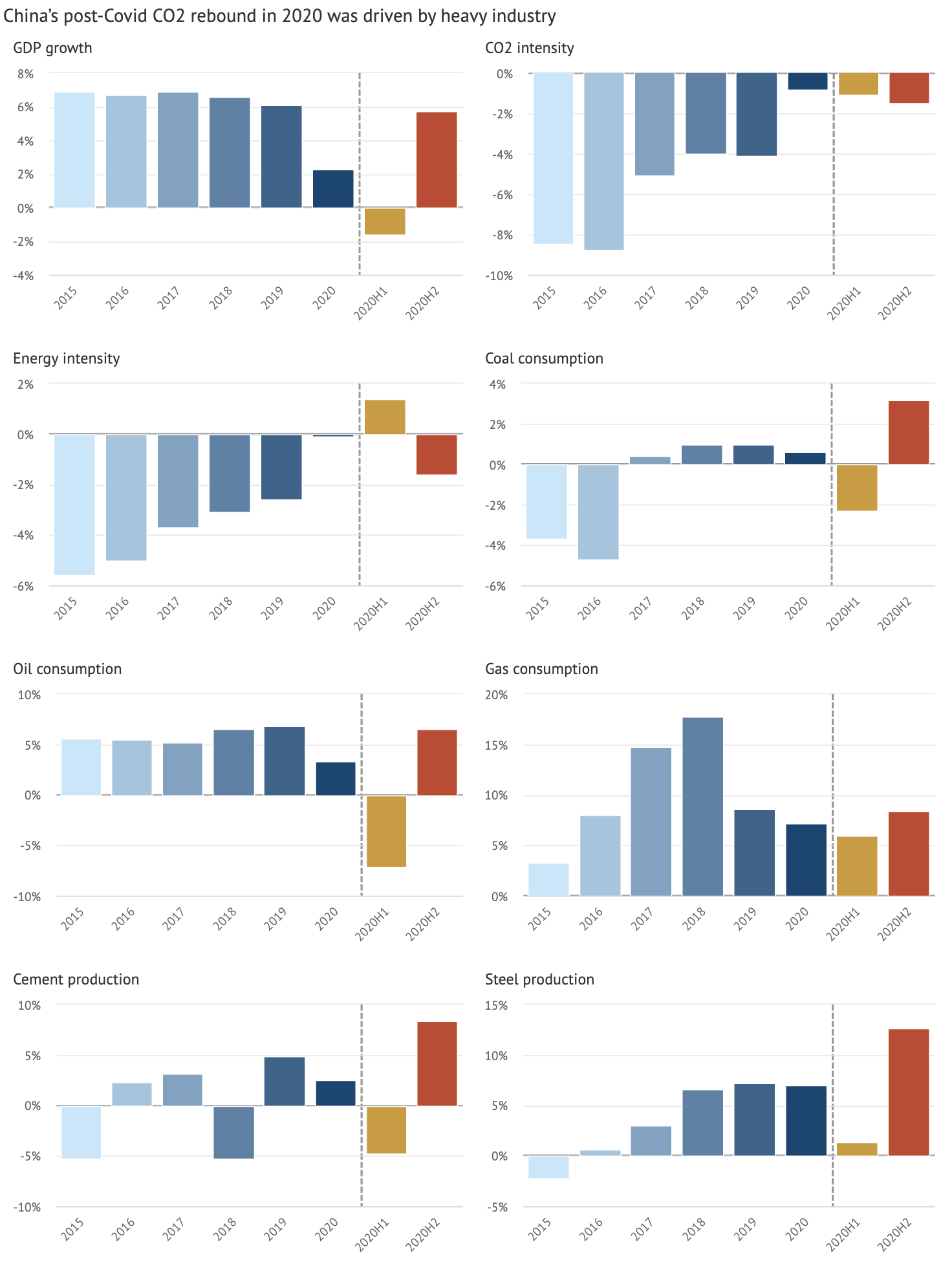

While emissions declined by 3% in the first half due to lockdowns, they increased by more than 4% in the second half. In total across 2020, CO2 emissions increased by 1.5% compared with 2019, based on analysis of the country’s annual statistical communique.

上微信关注《碳简报》

China’s return to economic growth after its first Covid-19 lockdown has relied on stimulating polluting sectors, such as construction and heavy industry. This saw the country’s consumption of coal, oil and gas all growing dramatically in the second half of the year, despite the pandemic and the government’s new pledgeTo reach carbon neutrality before 2060

The new data highlights the significance of China’s new five-year plan targets, due to be released at the annual legislative session starting on Friday. It is unlikely that the plan will set targets that would stop the increase in CO2 emissions. However, it will likely slow it down.

Steady emissions

In early 2020, severe lockdown measures to tackle the unfolding coronavirus pandemic saw China’s CO2 emissions drop by 10%Year-on-year in February and March However, emissions decreased as restrictions were lifted. quickly surgedPast pre-Covid levels, going onto to record an approximate 3% year-on-year increase2020, third quarter

Analysis of the full-year data in China’s new statistical release points to an even larger increase in the fourth quarter, pushing the overall total for 2020 to 1.5% above that seen in 2019. This is illustrated in the chart below. The first half of 2020’s emissions surge is highlighted in yellow, and the second half in blue.

Annual growth of China’s CO2 emissions, 2015-2020, calculated from the Statistical Communiques on Economic and Social Development. To show the effects of the economic shock from Covid-19 during the first half of 2020 and the recovery facilitated by heavy industry in the second half, the annual changes in 2020 have been broken down. Data from news reportsOn energy statistics for half the year and monthly industry information WIND Financial Terminal. Chart by Carbon Brief Highcharts.

Whereas the annual increase of just 1.5% continues the recent downward trend in China’s emissions growth, the surge in the second half of the year points in a different direction.

On the surface, the annual increase in China’s coal consumption also looks modest, at just 0.6% across 2020 – compared to growth of 1% in 2018 and 2019. However, this also hides a rapid rise in coal demand during 2020’s second half.

Since coal demand reportedly fell 2.3% in the first half of the year, full-year growth of 0.6% implies that consumption in the second half must have been approximately 3.2%, shown in the chart below alongside other key indicators of China’s energy and emissions.

Compilation of key indicators related to CO2 emissions, 2015-2020, from China’s annual Statistical Communiques on Economic and Social Development. To show the effects of the economic shock from Covid-19 during the first half of 2020 and the recovery facilitated by heavy industry in the second half, the annual changes in 2020 have been broken down. Data from June industrial statistics is used to disaggregate the first and second halves of the year. news reportsOn energy statistics for half the year and monthly industry information WIND Financial Terminal. Chart by Carbon Brief Highcharts.

Similarly, oil demand fell by at least 7% in the first half of the year (and demand for refined oil products fell 15%), according to official data – and OPEC estimatesA 7.1% decline in crude oil demand. In the second half of 2020, there was a 6.5% rebound.

The cement output fell by almost 5% between June and June, before rising dramatically by 8% in the second half.

There are major uncertaintiesThe first half of 2020 saw a decline in industrial and economic activity. Official statistics seem to have understated the contraction. However, the rebound of emissions in 2020’s second half is in line with other data sources.

The communique indicates that electricity demand increased by 3.1% in 2020 and thermal generation (predominantly gas and coal) by 2.1%. This suggests that the generation mix became slightly cleaner, even though power-sector emissions continued increasing. Solar and wind power generation grew about 15%, nuclear 5%; solar 9%; and hydro 4%.

According to the statistical communique in 2020, total energy use increased by 2.2%. Even if we take the official GDP number as a whole, this means that the country experienced a 0.1% improvement in energy intensity and a modest 0.8% increase in the economy’s CO2 intensity. These are the energy use per unit of GDP and the emissions.

The communique indicates that the increase in CO2 intensity is a round number of 1%. However, an exact figure can be derived from the reported increases at the consumption of oil, coal, and fossil gas.

What caused the increase in emissions?

The sharp rebound in China’s energy use and emissions output reflects the pattern of “dirty recovery” that has been emerging since mid-2020. Policymakers doubled down on the old playbook of stimulating the dirtiest and most energy-intensive sectors – construction, heavy manufacturing – to offset weakness elsewhere.

This pattern is evident in the statistics on steel production: crude iron output grew by 7% in 2020, and steel products grew by 10%, four times faster than GDP.

Steel production is the biggest emitting sector for both CO2 and air pollutants. It is also an indicator of construction volumes, as most steel is used in construction projects.

China’s policy response towards post-pandemic recovery has, thus, been distinctly differentFrom other countries, who supported household incomes as well as consumption through income transfer. This, in turn, has served to boost China’s export manufacturing industry.

China’s approach helped deliver a positive GDP number, but is a further setback to efforts to pursue “high quality” growthOr green the economy.

The failure of many local governments in enforcing controls on steelmaking and coal power is a contributing factor to the surge. Only enforcing 2020 steel capacity targets would have avoided 300m tonnes of CO2 emissions (MtCO2) per year, by a conservative estimate, equivalent to the overall 4% increase in China’s CO2 emissions in the second half of 2020.

(A recent, unprecedented environmental inspection of the National Energy Administration heavily criticised the regulators for expansion of coal power and energy-intensive industries in the eastern part of the country, where new capacity is supposed to be strictly controlled under the country’s air quality policies. See Carbon Brief’s detailed Q&A explaining the potential significance of the criticism for China’s climate policies.)

The pattern of China’s rebound differed starkly from expectations. The IEA had projected in April that China’s energy consumption would fall 4% in 2020, implying an even larger fall in CO2 emissions. The agency did not mention this. noted in NovemberThat means that emissions are on the rise.

What does the emissions surge mean for China’s climate targets?

China comfortably exceeded its 2020 target with a modest 0.8% increase in CO2 intensity. Copenhagen accord targetReports of a 40-45% decrease in CO2 intensity between 2005 and 2020 had already fallen48% by 2019.

This means the increase in overall CO2 emissions in 2020 remains consistent with China’s international climate commitments, under which it has left room for emissions to continue growing until the late 2020s.

However, an acceleration in emissions growth rate during the second half is not in line to the target of peaking emission. before 2030Especially as pledgeTo reach carbon neutrality by 2060, rapid reductions of emissions must be made after the peak.

Additionally, fossil fuel growth is not limited to short-term demand increases. It is built on the continuous expansion of long-lasting infrastructure.

China dominated investments in new coal power plants in 2020, opening three-quarters of the world’s newly funded capacity. It was also responsible for more than four fifths of all newly announced coal power projects.

A total of 38 gigawatts (GW) of new coal – about one large coal plant per week – was added to the grid and a total of 73GW of planned new projects were announced, while less than 9GW was retired. In the meantime, the number of new projects in the rest was down sharply.

All eyes on the 5-year plan

Xi Jinping, China’s leader, must have known that both the accelerating pace of fossil-fuel investment growth and the continuing and accelerating growth in emissions are facts that he had to be aware of when he pledged to reach carbon neutrality by 2060.

Therefore, Xi’s pledge could be read either as a domestic signal to turn around these trends – or an international one to put a green veneer on an economy that he thinks will continue to increase emissions until late in the decade.

The key indication of which way the leadership leans will be the energy targets for 2025 that will be released as a part of China’s 14th five-year plan.

The overarching plan will be released at the annual session of China’s largely ceremonial legislature, starting on Friday. This will include a limit on total energy consumption and a target for the share of non-fossil energy – the sum of renewable energy and nuclear.

Together, these two targets will largely determine the maximum level for China’s CO2 emissions in 2025, with a bit of give depending on the exact mix of fossil fuels.

In the second half of 2021 or early twenty22, a range of more specific targets will become available, including the specific plans to address energy, renewable energy, and coal, as well the CO2 peaking action program being developed by the environment ministry.

The surge in China’s CO2 emissions in the latter part of 2020 shows a clear need to manage growth in heavy industry and accelerate deployment of clean energy, if China’s goals to peak and decline emissions are to be met.

Some of this ambition already seems to be realizing with the installation of solar energy expectedThis year, we will reach 75GW new targets under considerationAfter record-breaking additions at 2020’s end, this would give wind power installations a boost.

Sharelines from this story

[ad_2]

Source link

{kind=link}