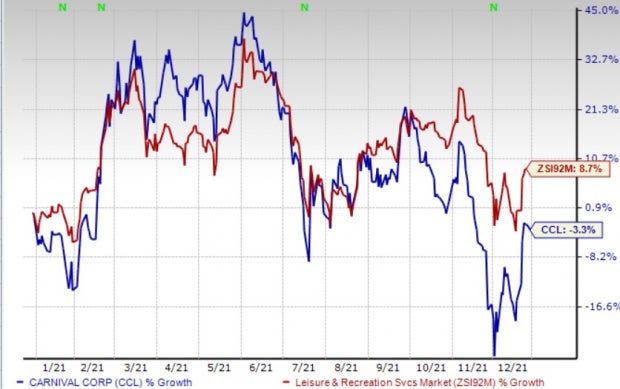

The year 2021 was difficult for cruise operators. Carnival Corporation & plc (CCL – This is not an exception. The company’s shares have declined 3.3% year to date, against the industry’s growth of 8.7%. But it is slowly getting out of the woods. It is looking good for a resumption in operations and better bookings. Carnival will continue to focus on fleet expansion in order to drive growth. Let’s delve deeper.

Key Growth Drivers

The company has resumed operations after the shutdown caused by the coronavirus. The company is also working to resume sailing from Australia or Asia. The company resumed cruise operations in fiscal 2021 with 50 ships (68%) of its fleet capacity. The company plans to bring its entire fleet back into operation by the spring 2022.

The company stated that both booking volumes and book positions are extremely encouraging. The bookings for the fourth quarter of fiscal 2020 were negatively affected by the Delta variant, but they have since improved and returned to preDelta levels in November. All future cruise bookings saw higher volumes than those in the third-quarter of 2021.

According to the company, cumulative advanced bookings for 2022 and 2023 were at the higher end historical ranges and at higher prices than 2019 levels. The positives were accentuated by the emphasis on price maintenance and comparable itinerary options. As of Nov 30, 2021 total customer deposits were $3.5 Billion, compared with $3.1 Billion as of Aug 31, 2021. The company plans to capitalize on the momentum and focus on advertising campaigns that include holiday activations for Christmas Day or New Year’s Eve.

Carnival is continuing to invest in fleet expansion to drive its growth. The company announced that it will soon add six LNG-powered ships and AIDAnova to its AIDAcosma system, which is used for travel to Germany. It also announced the additions of Costa Firenze (for Southern Europe), and Costa Toscana for the U.K. In addition to this, the company also added Rotterdam (for Southern Europe) and Mardi Gras (for the U.K.). According to the company, the addition of new ships and removal of less efficient vessels will likely lead to a 4% decrease in ship-level unit costs in the upcoming periods. This will increase the top and bottom lines.

The Zacks Rank #3 Hold company expects cash flow to be positive in the first half of 2022. It expects to produce higher EBITDA than in 2019 due to improved cost structure and additional capacity.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Concerns

The pandemic has been hurting the company’s operations and global bookings. The coronavirus crisis will likely cause delays in ship deliveries, as the shipyards have also been affected. It expects that a gradual resumption will have a material effect on all aspects of the company’s business, including its liquidity, financial position, and results of operations.

Keeping companies liquid has become a daunting task in the face of the pandemic. At the end of Nov 30, 2021, the company’s total debt stood at $33.2 billion compared with $26.8 billion as of Aug 31, 2021. It ended the fourth fiscal quarter 2021 with cash and cash equivalent at $9.1billion, compared with $7.2billion in the previous quarter. Although the company’s cash flow generation has improved sequentially, it may not be enough to manage the high-debt level. The average monthly cash burn was $510 million in the fourth quarter. At the end the fourth quarter fiscal 2021, the company had an average debt-to capital ratio of 0.6.

The Key Picks

Here are some stocks that rank higher in the Zacks Consumer Discretionary Sector. Electronic Arts Inc. (EA – Free Report Bluegreen Vacations Holding Corporation (BVH – Free Report Century Casinos, Inc. (CNTY – Get a Free Report You can view the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Electronic Arts has a Zacks Rank 2 (Buy). On average, the company’s trailing four-quarter earnings surprise is 11.7%. The shares of the company have risen 6.7% over the past month.

The Zacks Consensus Estimate for Electronic Arts’ current financial-year sales and earnings per share (EPS) suggests growth of 24% and 22.3%, respectively, from the year-ago period’s levels.

Bluegreen Vacations has a Zacks rank #1. The company has an average quarterly earnings surprise of 695%. The shares of the company have risen by 159.7% so this year.

The Zacks Consensus Estimate for Bluegreen Vacations’ current financial-year sales and EPS indicates growth of 27.5% and 199.3%, respectively, from the year-ago period’s levels.

Century Casinos carries a Zacks Rank #2. The company’s average quarterly earnings surprise for the trailing four quarters is 758.9%. The company’s shares have appreciated 99.4% this year.

The Zacks Consensus Estimate for Century Casinos’ current financial-year sales and EPS suggests growth of 26.9% and 146.6%, respectively, from the year-ago period’s levels.

{kind=link}