Kitzzeh/iStock Editorial via Getty Images

At the end of April, Unilever PLC (NYSE:UL) (OTCPK:UNLYF) released its Q1 trading report. Here at the Evidence Lab Towers, we haven’t really looked much at consumer staples in the past, but with levels of inflation which we haven’t seen since the late 70s and many consumers starting to feel a squeeze on the cost of living, we felt obliged to take a look – after all, staples are the most important thing in terms of consumption. (Side note – for anyone scratching their heads at the article title, Rexona is sold under the brand name “Sure” in Europe).

Q1 Trading Report Comment

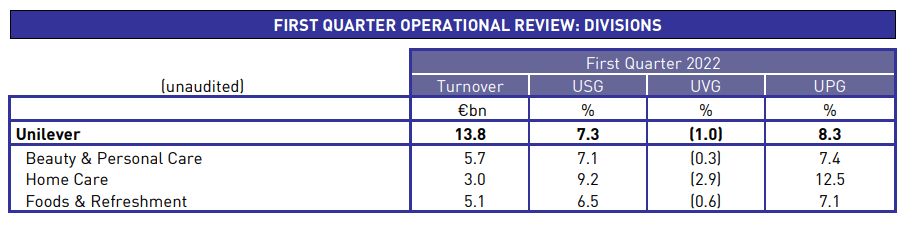

We felt like the best place to start was the Q1 results, or rather, the trading report. The first quarter went very well for the Company which recorded like for like sales growth of 7.3%, beating consensus. While this growth was mainly price driven, volumes were also better than expected, though slightly negative coming in at -1%, but beating the company consensus which stood at -1.7%.

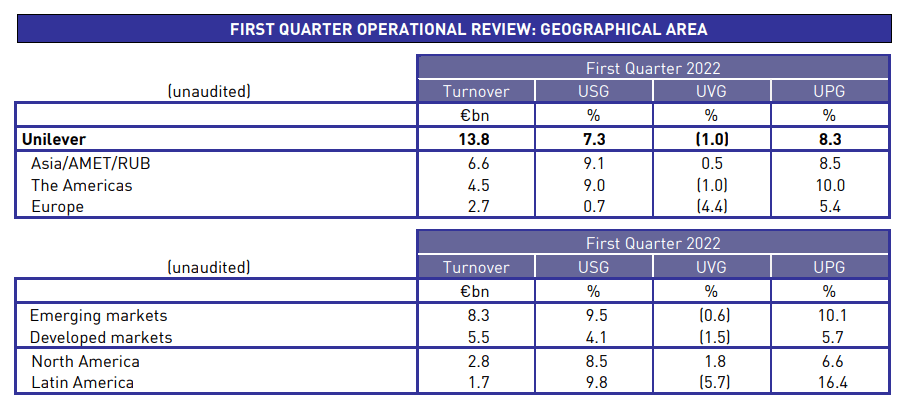

Below we have posted the Q1 turnover broken down on a segmental basis and also a geographical basis. Note Underlying Sales Growth (USG) as the sum of Underlying Volume Growth (UPG) and Underlying Price Growth (UPG).

Unilever Unilever

We can see that the company is less sensitive in emerging economies where although the price growth is higher, the volumes are impacted less.

“We are executing well in a very challenging input cost environment. Underlying sales growth of 7.3% was driven by strong pricing, with a limited impact on volume in the quarter. This performance was delivered against the backdrop of significant rises in input costs that have further accelerated through the first three months of the year, and the human tragedy of the war in Ukraine.” Commented CEO Alan Jope “The delivery of another solid quarter of sales growth builds on the improved growth momentum that we achieved in 2021 and is underpinned by Unilever’s increased focus on operational excellence as well as disciplined adherence to our chosen strategic priorities.”

Unilever also gave an update on their guidance for 2022, citing the war in Ukraine as a cause for higher than expected input costs for the second half of the year. This will cause the Group to take further pricing action and despite the very promising 1st quarter in terms of sales, they have not updated their guidance for ’22, expecting it to come in at the top of the range (4.5% – 6.5%). Operating margin guidance for the full year also remains unchanged at 16% – 17%.

Looking Forward and Conclusion

Unilever stated in their report that they expect a low single digit volume decline for FY 2022 as a direct consequence of increases in pricing. Speaking of which, at the end of Q1, Unilever has taken 68% of the pricing increases needed to restore margins. These are expected to be completed over the following two years as the Group takes further action on prices.

The key risk for the stock is that the impact on volumes from raising prices becomes worse than anticipated.

We see Unilever as a key value stock. The management confirmed the dividend, maintaining a healthy yield of close to 4%, whilst at the end of March, the Group commenced with its first tranche worth 750 million euros of a 3 billion share buyback plan. We value Unilever with an EV/EBITDA of 13.5x compared to a peer average of 17x. We don’t see any justification for this discount, especially considering the strength of Unilever’s brand portfolio. We assign a buy rating with a target price of $52.00 per share.

{kind=link}