Getty Images – da-kuk/E+

We are not surprised by a +6% price rise after Q1 results. Euronext (OTCPK:EUXTF), along with London Stock Exchange Group (OTCPK:LDNXF, OTCPK:LNSTYFor a more volatile environment, we recommend ( AfterThe Russian invasion and subsequent market turmoil. We reiterate our positive view of Euronext based upon:

- Borsa Italiana Group integration results in better than expected synergies

- Italian IPO Acceleration

- Due to strong cash flow, the DPS has increased to 1.93 per share.

Q1 Results

We were once again looking in the right direction, even though it meant being repetitive.

Euronext Q1 Results

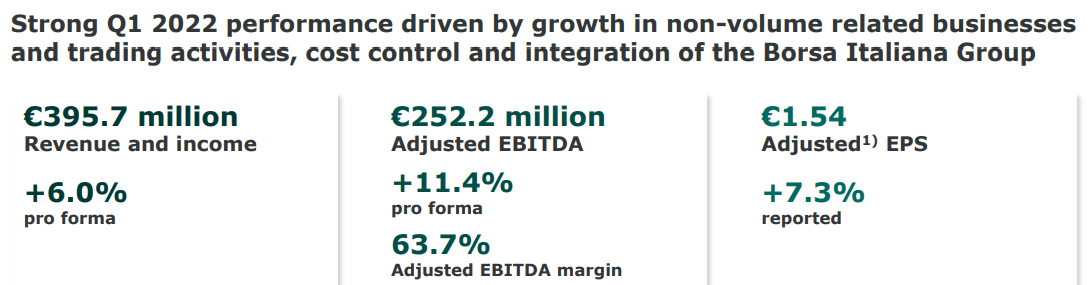

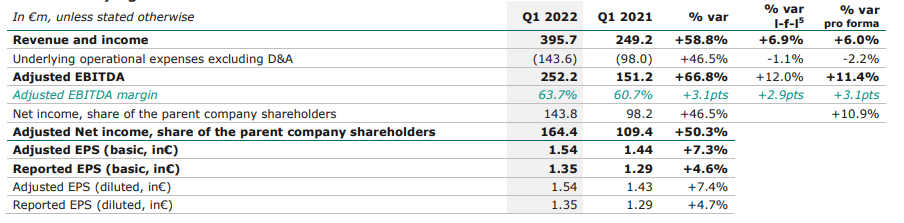

Borsa Italiana’s integration in Euronext continues to drive the positive results shown in the company’s quarterly reports. The group that combines the lists from Amsterdam, Brussels and Dublin, Lisbon Lisbon, Oslo Paris and Milan, raked in revenues of 395.7million, an increase by 58.8% for Q1-2022. This was a record quarter. This was a pro forma comparison. The Italian stock exchange had only been consolidated for eight of the previous years. The first quarter adjusted EBITDA grew by 66.8% to 252.2 million. This was due to both volume growth and cost discipline. Net profit increased by 50.3%, to 164.4million, and adjusted earnings per share rose 7.3% to 1.54.

Euronext Q1 Results (Q1 press release)

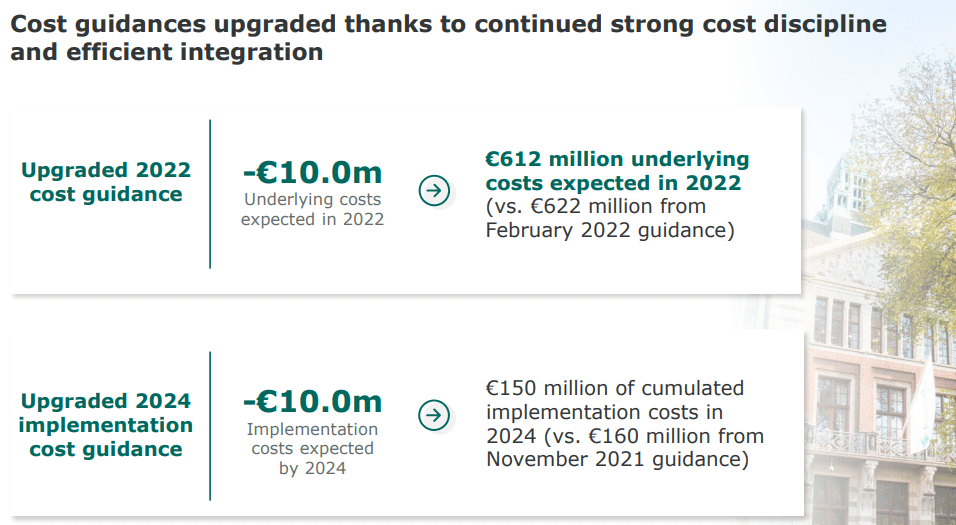

Euronext has updated its guidance on costs for 2022. It now anticipates 10 million fewer in underlying costs (612 million total) and 10 millions fewer in implementation costs (now 150million).

Euronext Cost Synergy Update (Q1 Results)

As we were forecasting (using VIX as a proxy), revenue has been growing in the first three month. This is due to trading on exchanges.above average” Giorgio Modica, CFO, confirmed the factFurther explained as “High volatility is the driving force” In April, cash transactions averaged 5.7% more than in the same period last year. The Russian invasion of Ukraine marked the first quarter.The business model of Euronext It has remained resilient”Boujnah, CEO, confirmed that “o” was also being used.Russian exposure to Ukraine is negligible“.

Conclusion

The company reaffirms its commitment towards achieving successful integration and maintaining cost discipline. The data center migration from Basildon, Italy to Bergamo was confirmed in this regard. Customers have confirmed that Euronext is ready to begin the migration as planned. Connectivity tests have been conducted with customers.

Concerning the valuation, based upon the latest results, we adjusted synergy and we keep our buy rating. A P/E based in FY2023(E), arriving to a new value at 100 per share (previously: 98 per shares), gives the entity a 29% upside for anticyclical companies, without taking into account a dividend return of 2%.

You can find our past articles on European stock markets in our publications.

{kind=link}