AsiaVision/E+ via Getty Images

Thesis for Investment

MercadoLibre, Inc. (NASDAQ:MELIRecently, ) reported strong FQ1’22 earnings cards. It validated the company’s thesis that LatAm’s e-commerce growth and FinTech (offline, online) growth are still in its early stages. MELI’s solid performance is notable.Amazon () is a sharp competitorAMZN) and its US e-commerce peers in Q1. The US ecommerce players continue to experience significant growth deceleration as well as higher costs. MercadoLibre managed to weather the difficult comps in FY21 thanks to its well-diversified business that spans its ecommerce and FinTech ecosystem. Notably, MercadoLibre’s offline FinTech company also benefited from this reopening.

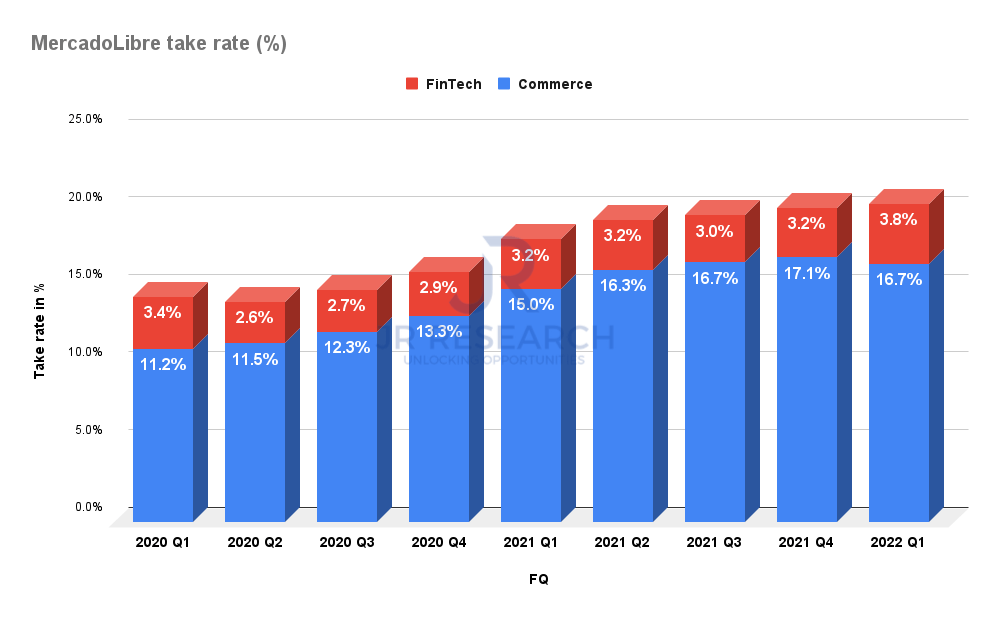

MercadoLibre’s take rates have remained high, demonstrating its pricing leadership. It has also helped weather the difficult rising inflation and interest rates environment in LatAm.

MercadoLibre may not be immune to these macro headwinds. However, management is confident that the company can overcome them. It would also be investing heavily in fulfillment and headcount to increase its competitive advantage.

MELI stock has traded at a premium despite its proven growth capabilities. We believe the stock will continue to trade at a premium, but we don’t anticipate a significant re-rating in near future.

We reiterate our Buy rating on MELI stock. To reduce risk, we encourage investors not to buy in bulk.

MELI Stock Is Still Available at a Premium

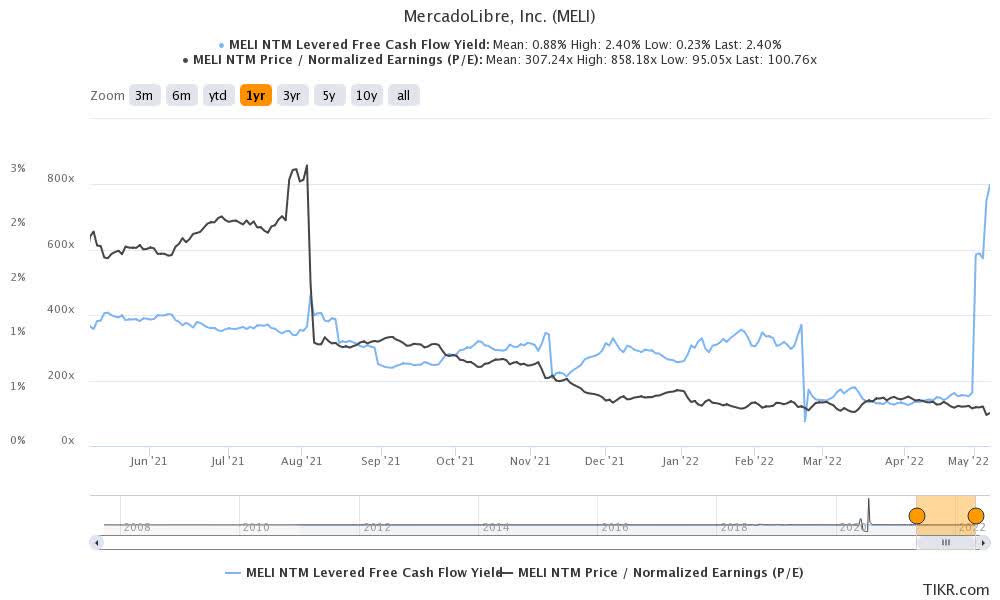

MELI NTM FCF yields 0.5% and NTM normalized PE (TIKR)

MELI stock is a stock with an embedded growth premium. There should not be any doubt about that. It was last traded at an NTM standardized P/E 100.76x. However, its NTM FCF Yield has improved to 2.4%. Stocks with a high growth premium continue to face harsh market conditions.

MercadoLibre has been able to continue its success despite the challenges of macros and a more competitive market. Investors were understandably skeptical about its growth premium. MELI investors have been subject to volatility as the price discovery process continues.

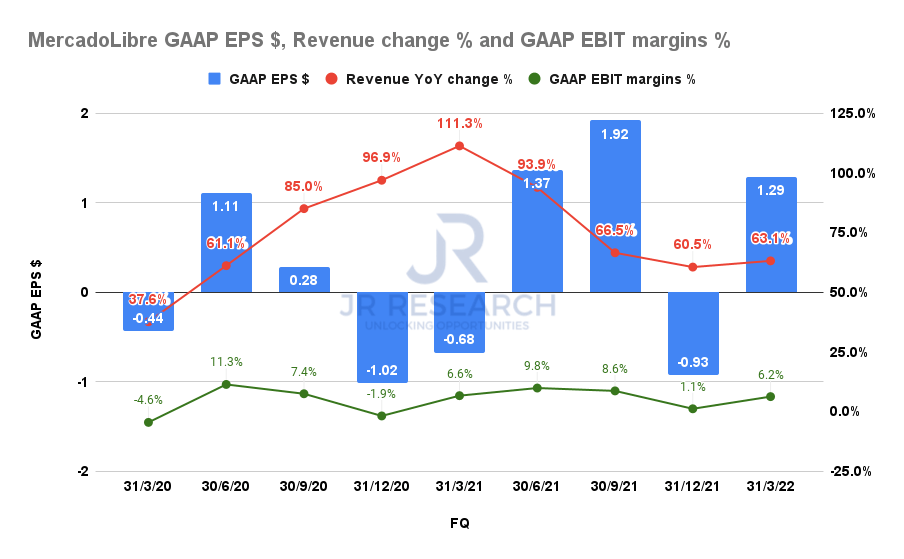

Its Q1 results were solid, but its margin was less than expected.

MercadoLibre revenue, profitability (S&P Capital IQ)

MercadoLibre reported FQ1 revenue of $2.25B, an increase of 63.1%. It easily beat the consensus estimates of $2B and was up 44.6% YoY. This was remarkable considering that the company had a record FQ1’21, when its revenue rose by 111.3% YoY. Investors were also concerned by the slowdown in the company’s revenue growth since FQ1 21. Investors were also concerned about FQ1’s slowing revenue growth since FQ1’21.

However, its EBIT margin decreased to 6.2%, from 6.6% the year before. Telegraphing that it would have to deal with higher OpEx and a larger provision for credit losses due to its growing loan portfolio, the company stated that it was able to do so. The company is confident with its underwriting standards as the company expands its loan portfolio. Pedro Arnt, CFO, stated (edited).

When we look back at our achievements in a difficult environment, we have been able grow originations and increase the size of the book at a good rate. We believe that our underwriting is aided by the data we have on consumers, our touchpoints with them, and our collections operations. I believe that we must deliver on that and continue growing the books in line to our confidence in underwriting. Then we’ll see how things develop going forward. All signs are positive so far and everything is going according to plan. (MercadoLibre FQ1’22 earnings calls)

Investors Must Pay Attention to Its Take-Rate Trends

MercadoLibre take rates % (Company filings)

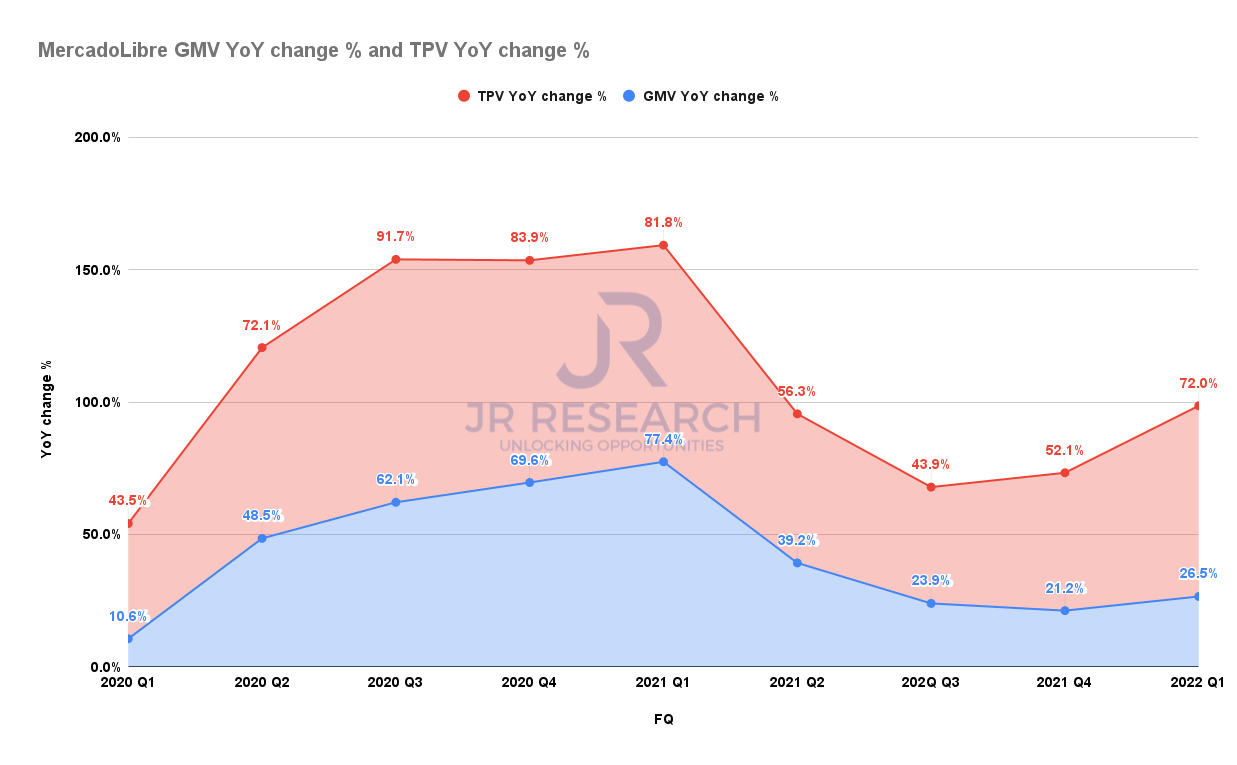

MercadoLibre GMV Change % and TPV Change % (Company filings)

MercadoLibre’s topline growth has been supported by its ecommerce and FinTech segments. Investors should be aware that FinTech (43.2% of Q1 revenue share) has grown faster but e-commerce is still its main revenue driver.

FinTech could expand much faster with the expected normalization and expansion of its offline payments products, however. We also noticed that the total payment volume (TPV), increased by 72% YoY, while the e-commerce gross merchandise (GMV) grew only 26.5% YoY.

E-commerce is still more profitable due to its higher take rates. Despite this, its ecommerce take rate dropped QoQ from 16.7% to 16.7%, despite it being higher than the 15% it posted in FQ1 21. In addition, the FinTech takerate has increased. These increases were necessary to offset higher funding rates and higher provisions for credit losses in the current interest rate environment. We urge investors to monitor the changes in its take rates as they could have a significant impact on MercadoLibre’s consistency and profitability.

Is MELI stock a buy, sell, or hold now?

MELI stock is still vulnerable due to its embedded growth bonus. We remain confident that MELI’s solid execution in a highly competitive environment has proven the robustness and viability of its business model.

We ask investors to layer in their purchases despite the inherent volatility that MELI stock presents.

As such, we reiterate our Buy rating on MELI stock.

{kind=link}