Ceri Breeze/iStock Editorial via Getty Images

Author’s Note : This is a reduced and free version of an article that was posted on Alpha on May 3, 2022.

Veolia (OTCPK:VEOEY) is a simple company, on the surface of it. Its three service/businessSegments are essential to daily human life. This is one of my favorite qualities when it comes to investments.

We’ll be deconstructing the company, trying to understand it, as well as what we might expect if we invested in the company.

Veolia – Business Specifics

The company is a former member of the Vivendi conglomerate, and has a history that spans nearly 170 years. The business focuses on areas that have been or are currently under the control of the government.

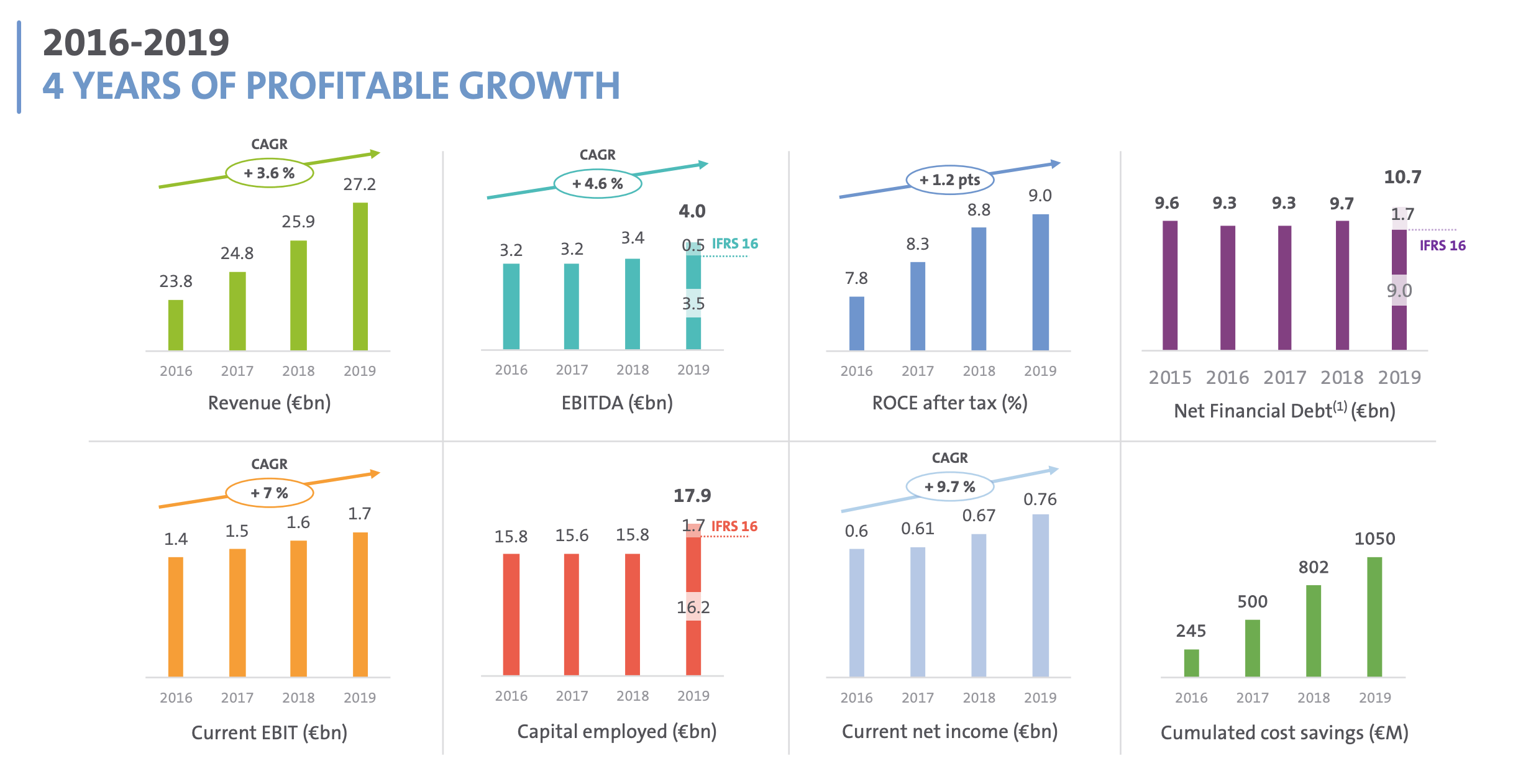

Veolia Growth history – Veolia IR

Although the company’s market capitalization is close to 20B this is only a small fraction of the global market. Greywater/waste markets are very fragmented, with both private and public players. Veolia, although it is a huge company, represents less than 5% in the global greywater/waste market. However, Veolia’s financial records clearly show the potential for economies of scale in this business.

Veolia Waste (Veolia IR)

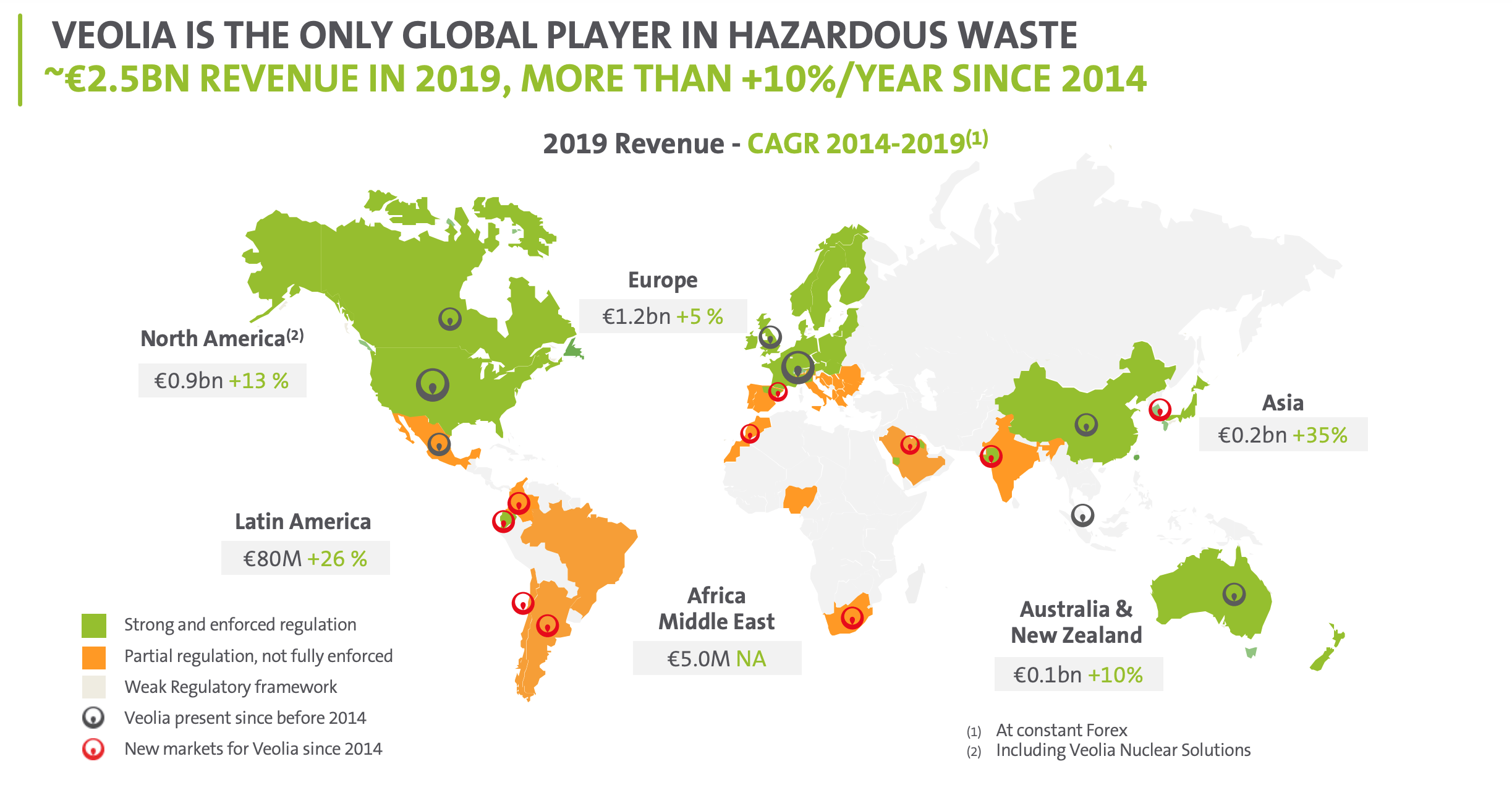

Recent consolidation in the market has been seen with the entry of Chinese players, who have taken over European capacity in this space, such as EEW or Urbaneser. Veolia itself has been active in M&A’ing here, which we’ll go into.

These are the key points of operations for the company:

- WasteThe company collects both hazardous and solid waste. This business is driven both by regulations regarding waste collection and recycling, as well as the growing demand for its services from emerging markets. The company seeks out these opportunities to maximize its efficiency in collection, treatment, and expand its operations in Asia and China. According to the company, this will ensure that there is future growth.

- WaterThis segment focuses on the entire water value cycle. It covers the management, production/sourcing and supply of wastewater. These legacy operations are based on comfortable margins and long-term contract regulations with French municipalities. We have seen the effects of a pandemic on these prices and contracts in France and China, and we know that there is no way to impact long-term margins with any of its operations, even during the worst.

- In EnergyVeolia is the manager of a network cooling networks. This segment is dedicated to helping customers achieve energy efficiency. This is a high-margin, asset-light business area that the company considers part of its growth vector due to increased building efficiency regulations. This is a touch on Proptech. I wouldn’t be surprised if they went deeper.

Geographically, the company is a traditional central European operator that is expanding into emerging markets in search of growth. Its growth and expansion are supported by the solid foundation of its mature markets.

The company plans to expand its operations in the mature areas, which account for more than half of its operations. Asset-light Service BaseThe company aims to increase its presence in emerging markets while maintaining its margins. assets to establish margins, and operations.

Veolia Dividend/ROCE (Veolia IR)

This theoretically is a great way to manage operations such like this and offers the company good potential for growth. France makes up 30% of the company’s operations. Europe accounts for 30%. Asia and other regions account for around 40%.

At a high-level, it is fair to say the company is heavily dependent on macro, GDP, or similar-level developments. Although there is a baseline volume and demand for water and waste, we still need to have a minimum level of service. However, things in Energy are a little different and so are the company’s expansion plans.

The company is sensitive to fluctuations in energy prices. This affects both the company’s pricing and income from waste treatment. Water, however, has pricing and sourcing conditions that are more stable and margins that are also more stable.

After deliberation by elected members of the municipal council, most markets have the municipality setting the water price. This takes into account variations in various factors, such as inflation and wages.

A company can also experience FX volatility because of the many markets it is involved in. Emerging markets account for between 30-35% of the company’s revenues and income. This means there are ups and downs that must be considered.

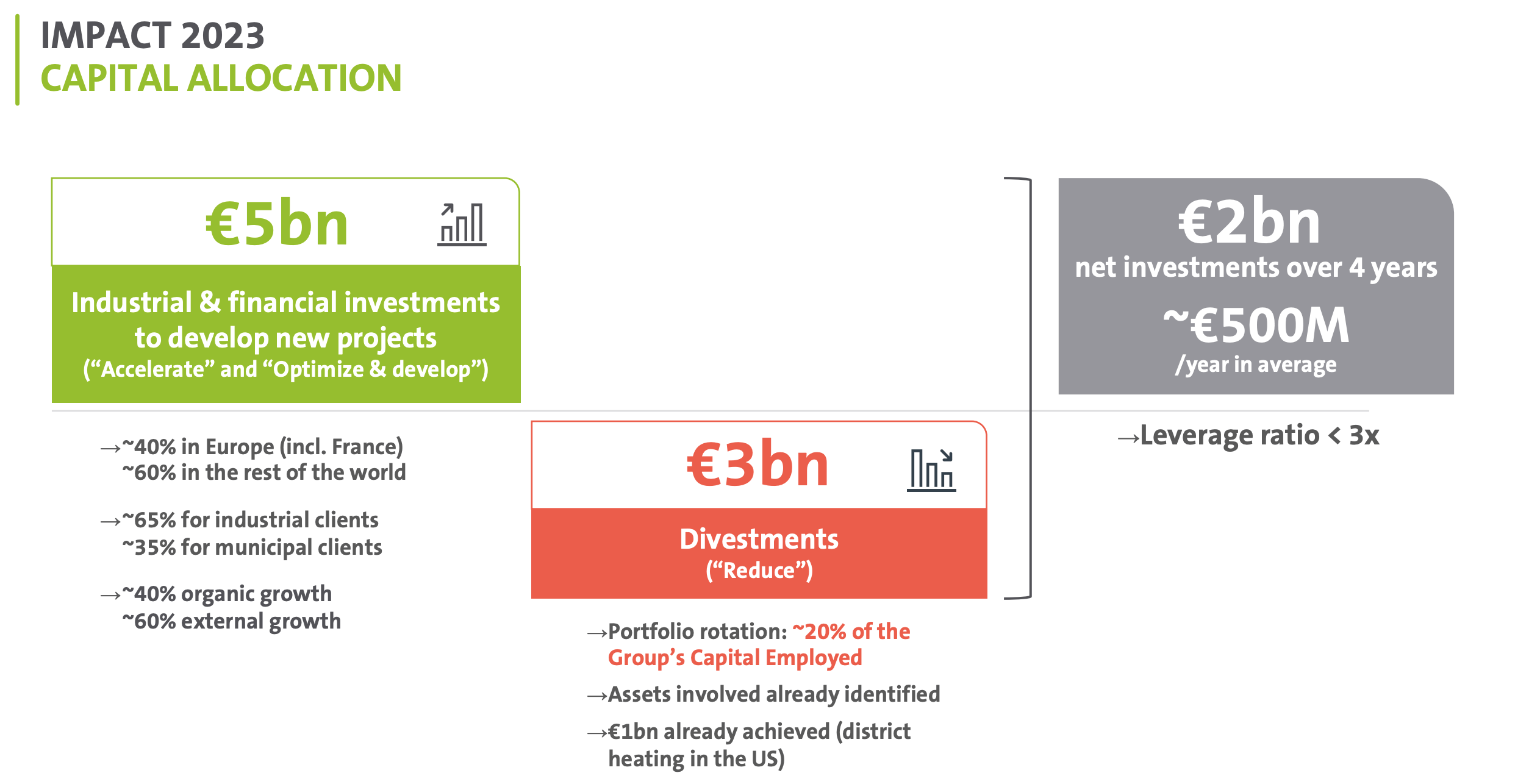

The company had a plan for a successful capital allocation strategy.

Veolia Capital Allocation (Veolia IR).

The upsides of the company are very obvious, at least from what I see. Veolia is a significant player in both the legacy and emerging critical areas like water, energy, waste, and energy. The recent merger of the company with SUEZ creates a transformation forcehouse in many areas and assets that overlap.

Veolia/SUEZ (Veolia IR)

The company reported solid numbers in 2021. The company reported a solid set of 2021 numbers. Revenue was up almost double digits and EBIT/EBITDA rose between 20-40% YoY, as the pandemic was over. The company increased the dividend by almost 43%, and net income was up more than 100%.

Positive price and volume impacts in the core areas of the company were key drivers of results. This surprised no one, and had a significant impact on company debt.

The company is still in debt following the closure of SUEZ. The expected guidance for the company calls for a 4-6% organic YoY EBITDA and a 6.2B EBITDA expansion. It also plans to increase the 2022E dividend from 1.22 per share. The expected leverage ratio (3X) calls for a reduction of several hundred billions of dollars in debt, but the numbers seem logical when you consider the 2021 results. The company’s guidance for 2022E is solid and realist. I expect the 2022E will be largely in line with company expectations.

Veolia can be described as “safe” on the fundamental side. We have solid ratings and numbers, as well as operational safety in the segments it operates. The company is investment grade rated and has a net interest/EBITDA of about 3.5X for the past year. It is expected to dip towards 3X in future.

As I have shown, the company has a long tradition of dividends. The yield is actually quite good, with a range between 3-4% and 3.5% for the 2021 dividend. This yield will increase to 3.7% at the 2020E if things pan out as expected.

Overall, SUEZ contributes more than 10B to Veolia’s company sales. These sales are expected to reach over 40B company-wide in 2023E. Going forward, the company’s earnings will increase significantly and dividends will grow to a level where we have a 5.5% yield on 2024E’s share price.

Veolia has a lot of things I love, and that is why I recommend the company.

It certainly has mine.

Veolia Risks

Veolia has some risks. We’ll be discussing these risks here. As I mentioned, the company is strongly correlated with GDP, infrastructure expansion and population growth. There are a few other things, too.

I will describe the management and board of the company as a weakness. French companies sometimes fall short of international ambitions. The board has been slow to take on this responsibility, instead of being content for a long period with the company’s slow-moving national markets. This is changing, but it’s important to note that French and German boards need to be vigilant to avoid becoming lax. Veolia has been lax for a while.

Another risk is the lack growth in mature operations of the company, which has very limited earnings growth potential. The proptech/service/energy segment will perhaps be able to deliver some growth, but overall, the companies’ mature markets are relatively low-growth.

Some will argue that the company doesn’t have an ESG. I disagree. First, ESG is not central to a company working with water and recycling, though this argument can be made. Second, I believe the company does what is required in terms ESG.

The company has very little exposure to Russia and Ukraine, accounting for less than 0.3% and 0.5% respectively of its revenues. While there are some energy-related exposures, including gas-fired assets (which are small), these are not significant.

Let’s examine the company’s overall market value.

Veolia’s Valuation

Veolia’s valuation story is very interesting because the company is currently being grossly underestimated. There is upside to this company no matter which perspective you take.

My DCF analysis is more conservative than the consensus. I expect a 3% increase in sales, EBITDA and CapEx, as well as overall growth across the board. With a WACC figure of 6.43%, the ROCE of the company is above this. This results in an implied DCF, based on conservative numbers around 36/share.

There aren’t many peers that could be considered for the company. American Water Works (AWK) and United Utilities (OTCPK:UUGRY). We also have FCC and Hera in Europe, as LYDEC. However, this company has a smaller market cap.

I believe that DCF and NAV multiples provide the best view of the company. I weigh Yield, P/E, and book multiples, but if there is weak peer-group correlation, they are lower. All of this leads to a conservative valuation of about 35/share.

This is actually lower than the average target here, including equity analysts like Alpha Value (Source : Alpha Value), who seeks a 40.8 PPT for the company. I feel more conservative here. My PT is closer to the S&P analyst average – but actually below even that.

13 analysts expect Veolia’s stock to trade between 27 and 43.4 with an average of 35.9. This gives us a potential upside of 25-28% for Veolia, which is not far from what I see.

I believe this company has significant upside at a price below 30/share. That’s why my PT is at this level.

I consider this a “BUY”, with a solid upside, and you should consider Veolia as an investment.

Thesis

Veolia is a great company in many great fields. They have excellent moats, a solid past, and great future prospects. The SUEZ M&A only strengthened the company’s next few years.

There are downsides as well as risks. These risks and downsides are small at this valuation. This company, with such operations, is at this price. This is exactlyThe type of investment you might want to make.

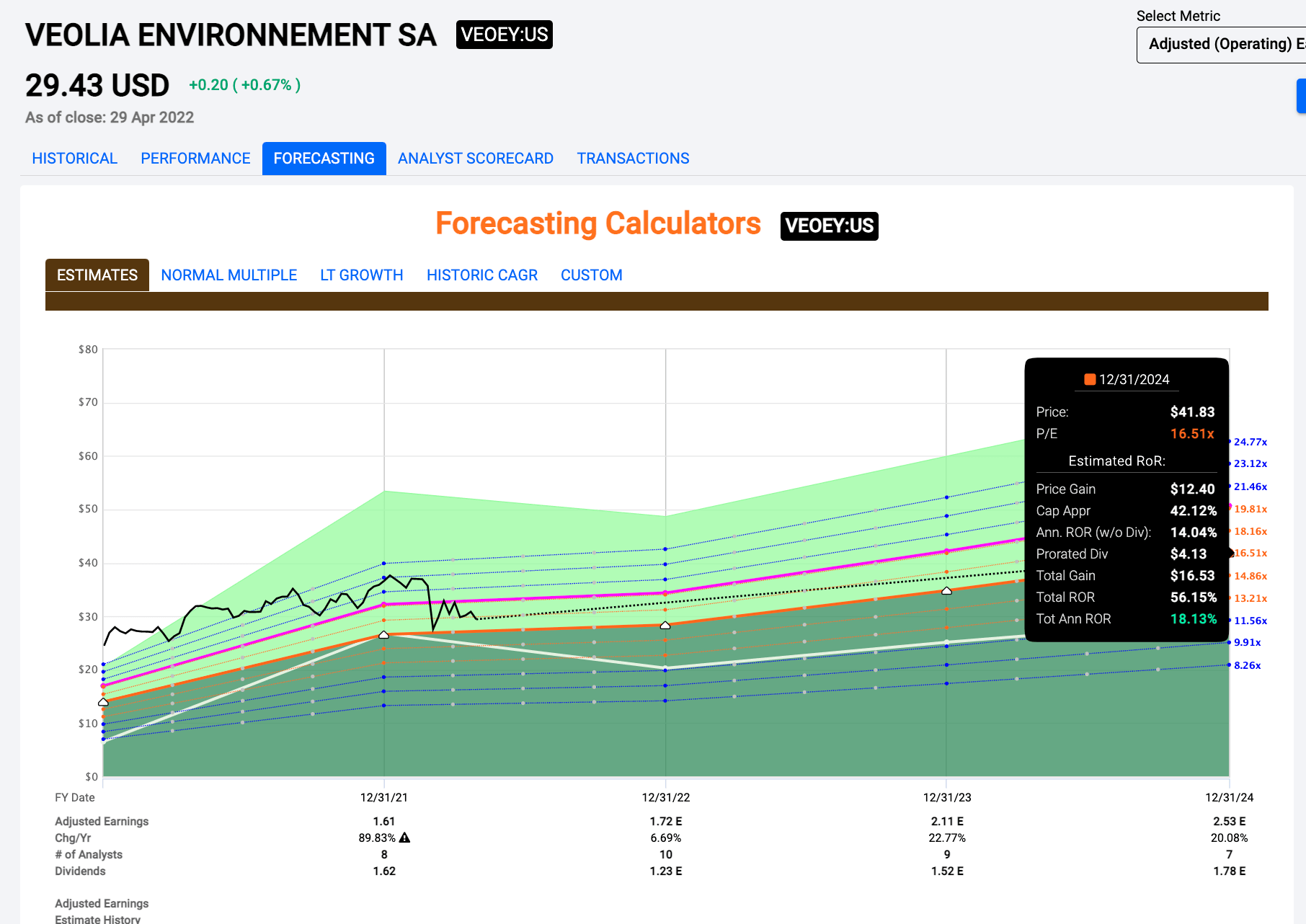

The NYSE receipt is known as VEOEY on the basis of the ADR. It is a 1:1X ADR. It is relatively liquid and trades at a range between 17-23X per share. Even at a conservative 16X per cent, the upside to the investment is substantial.

Veolia Upside (F.A.S.T Graphs).

This upside can even go up to 25-30% if we allow for a premium valuation or even higher, historically-accurate EPS growth. Veolia is an undervalued company in the water/waste/energy sector.

I believe that the upsides we have here far outweigh the potential forecast accuracy risk and the Veolia-specific risks. Although it might not be the best investment, it is definitely one of the most attractive.

My official PT is 35/share and I’m at “BUY”.

We are grateful for your time.

{kind=link}